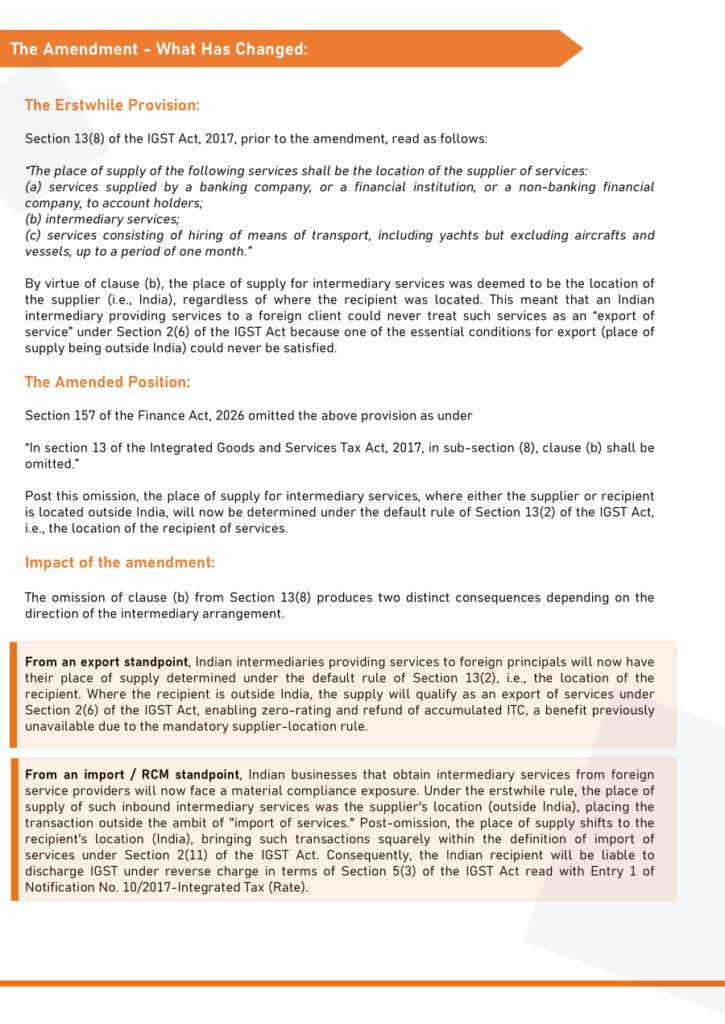

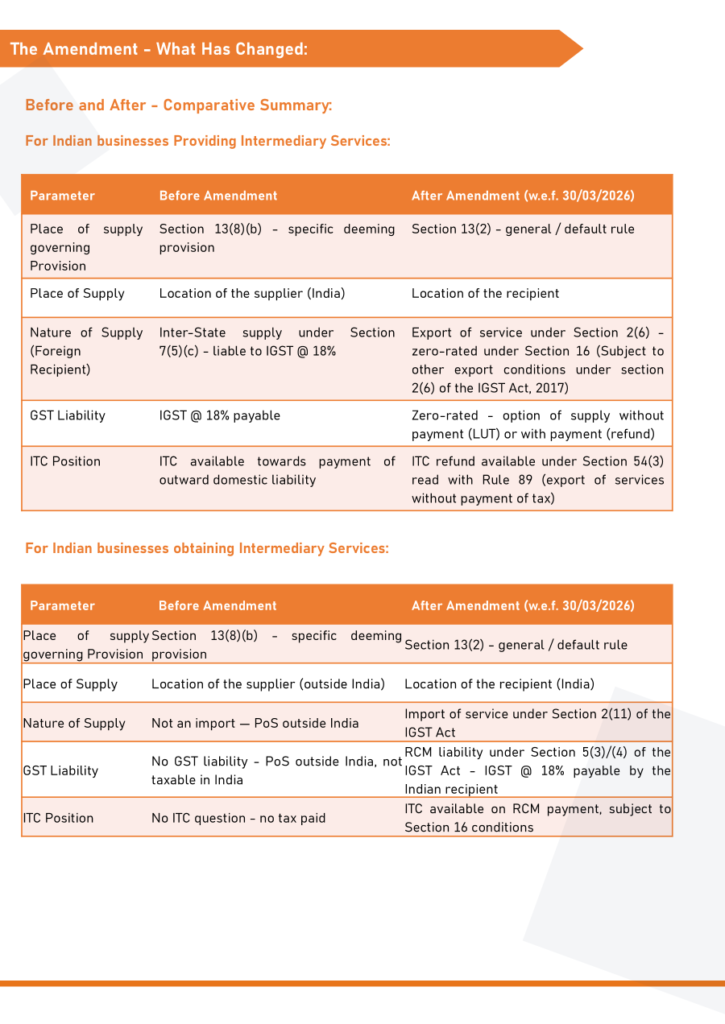

The recent omission of Section 13(8)(b) from the IGST Act, effective from March 30 2026, marks a pivotal shift in India’s GST landscape for intermediary service. By shifting the “place of supply” from the supplier’s location in India to the recipient’s location abroad, this reform allows Indian intermediaries to finally qualify for zero-rated export benefits and tax refunds

However, this change also introduces a new compliance mandate for Indian businesses importing these services, who must now discharge 18% IGST under the RCM